Resources on the Patent Revenue Budget Model

The University of California, like other research universities, requires all employees and other personnel who use university research facilities or resources to sign a Patent Acknowledgment as a condition of employment or visitor status. The University thus owns inventions that are made using university resources and facilities, but revenue from these inventions is shared between the university and the inventor. Distributing this revenue involves a complex model of allocations from the UC Office of the President (UCOP) and from the campuses to multiple stakeholders: inventors, UCOP, central campuses, and Offices of Research.

Considerations and Principles

There are several reasons that the allocation of patent revenue is highly complex compared to other modules of the UC Davis budget model. The funding stream allocated under the UC Davis budget model is a portion of a larger funding stream allocated by UCOP that is shared between campuses, individuals, and UCOP, with some share of funding coming to stakeholders from both models rather than a relatively simple proportion of an easily identified pool of funding.

Timing is also an important consideration. For one, it can take years for a patent to generate revenue – if ever. Moreover, expenses and deductions from multiple patent fiscal years are incorporated into the annual allocations received from UCOP. Extraordinary legal expenses can occur that are so great, the cost must be amortized, so offsets to income can take years to pay down. Revenues and expenses are also unpredictable from year to year, and therefore so are the net gains and losses.

In order to accommodate these considerations, UC Davis’ principles in allocating patent revenue are as follows:

- Ensure net revenues support all departments with patent activity, including those that have

expenses in excess of any royalties. - Pool all expenses and revenues since:

- Not all patents generate positive income streams

- UCOP allocations cross multiple patent fiscal years

- Departments and Principal Investigators should not have a disincentive to file patents to protect UC’s intellectual property out of concern that the university would incur expenses.

- Amortize extraordinary expenses in a given year to provide more dependable annual allocation to Units.

UCOP Patent Allocation Model

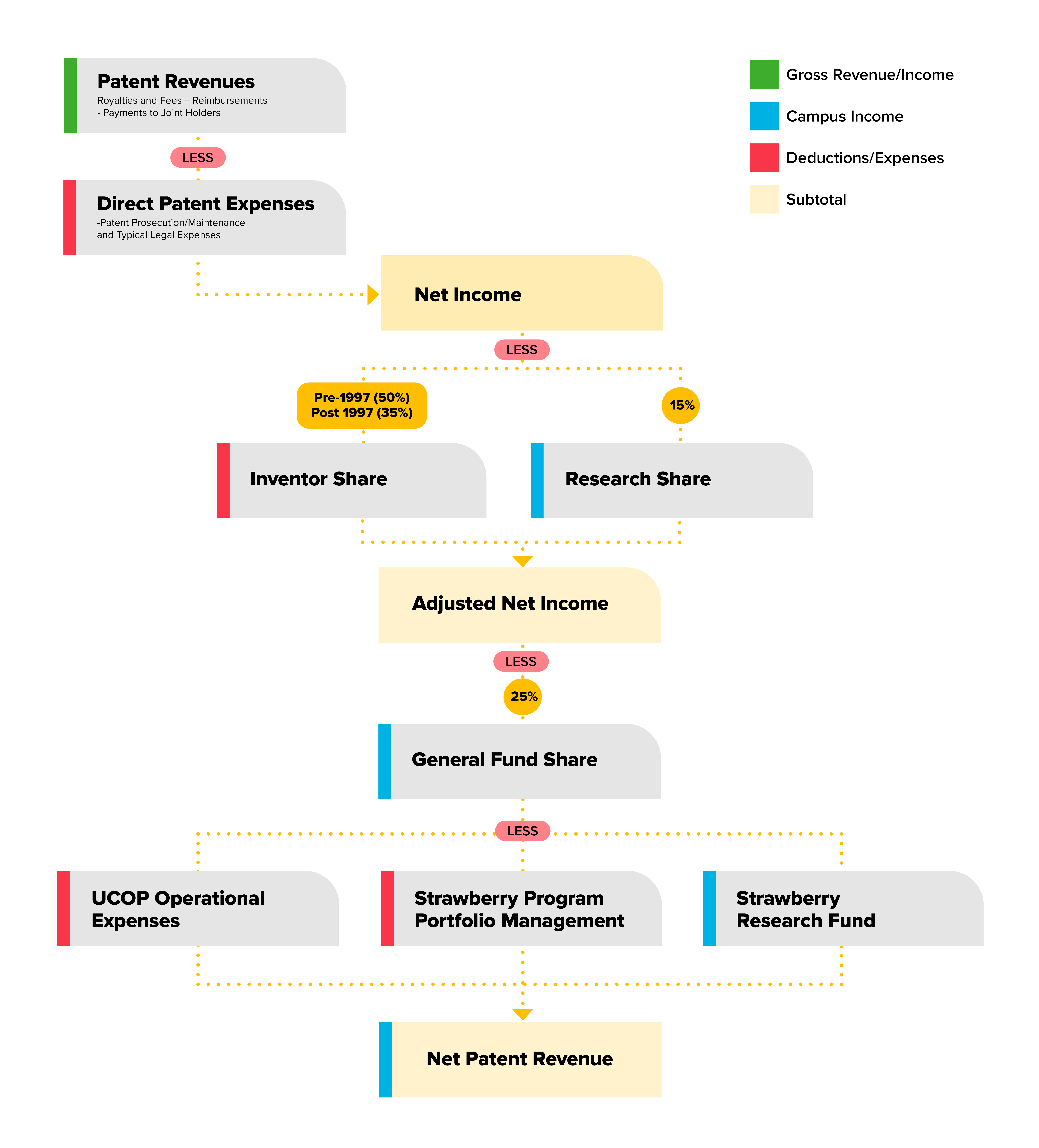

Per UCOP policy, the University agrees, following assignment of inventions and patent rights, to pay inventors 35% of the net royalties and fees per invention received by the University and 15% of net royalties and fee per invention for research-related purposes to the inventor's campus. Additionally, for UC Davis, a share of funds related to high-value strawberry patents are removed from the funding stream to the central campus and are treated specially, as described in the paper linked in the resources section below. The UCOP Patent Allocation Model is shown in Figure 1.

Figure 1. UCOP Patent Allocation Model

UC Patent Allocation Model (PDF) | Text Alternative

The pool of patent revenue funds (1) for distribution begins with the income from patent revenue and the licensing or royalty revenue associated with it, offset by payments to joint holders (i.e., non-UC entities who also hold some claim on the patent) and direct expenses, typically legal and patent prosecution expenses. Legal expenses are variable and may be quite high in some years.

Of this net income (2), inventors receive their portion (35% under the most current policy; 50% for employees who joined the university before 1997) of net income based on prior year income. In addition, 15% share of net income is to be returned to the campus to further research-related purposes (except in the case of patents predating 1990 at which time there was not a research share allocation). The remainder is the adjusted net income.

Of the adjusted net income (3), 25% is directed back to UC Davis as a contribution to state general fund pool. The general fund share was established by the UCOP Funding Streams initiative in 2011 and recognizes the State’s contribution to the university and how State funding supports faculty salaries and research that results in patents. Also deducted from adjusted net income are staff and software expenses for UCOP’s Office of Technology Transfer which supports tracking of patent prosecution expenses and revenue streams. Unique to UC Davis are additional deductions for UCOP staff expenses in support of our strawberry patent portfolio and a Strawberry Research Fund share that is allocated to the College of Agriculture and Environmental Sciences. The remainder is the net patent revenue (4). UC Davis receives the annual net patent revenue from UCOP late winter quarter and distributes the following fiscal year according to its own patent revenue budget model.

As just described, several of the deductions to reach net patent revenue are then allocated to the campus. The annual allocations from UCOP are broken into several line items to ensure each stakeholder receives the appropriate funding. In addition to the net patent allocation to be distributed per the campus budget model, (4) in the description above, the campus also received three other pools of funds to distribute on campus. These include (A) the research share, to be allocated to the campus to further research-related purposes; (B) the general campus share, which, per the UCOP budget model, is to be retained by central campus to support academic salaries; and (C) the Strawberry Research Fund, to be allocated to the College of Agriculture and Environmental Sciences. The Bayh-Doyle Act obligates the campus to utilize these patent revenues to support research and education at the University.

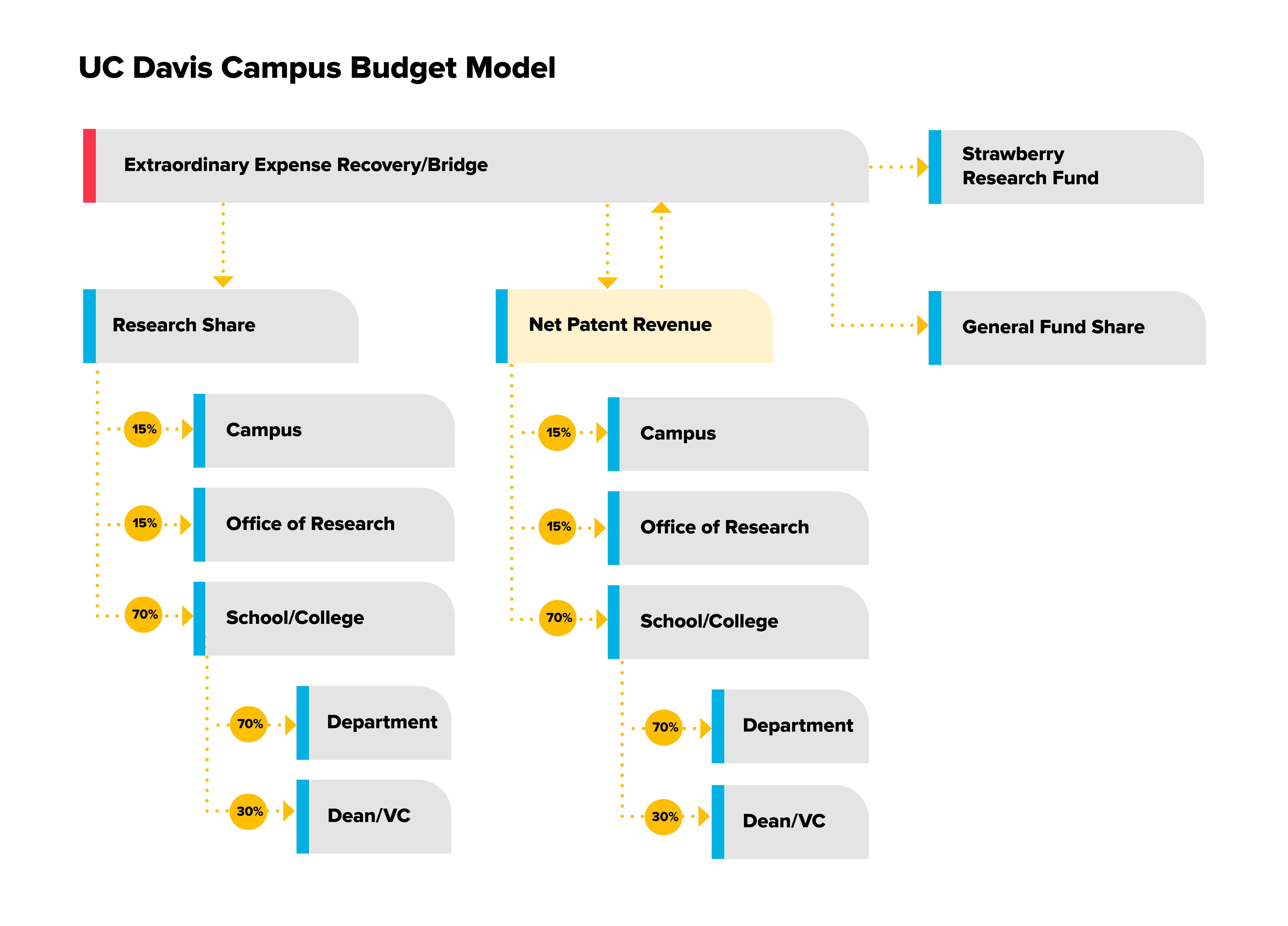

UC Davis Patent Revenue Budget Model

Of the line items allocated to UC Davis from UCOP, the UC Davis patent revenue budget model pertains to item (1), the net patent allocation, and item (3), the research share. The distribution of both follows the same fairly simple model. Of each line item, funds are split 15% to the Office of Research Innovation Access, 15% to the central campus, and 70% to the colleges and schools. The college, school, or unit share is then split 70% to the departments and 30% to the Deans’ or Vice Chancellors’ offices, as shown in Figure 2 below.

Note that effective with the 2018-19 allocations, the amount of net patent revenue available is adjusted to account for the Extraordinary Expense Recovery mechanism. In brief, this mechanism provides funding on a temporary basis to offset extraordinary expenses that would otherwise materially impact the patent revenue budget model in a given year. In years with no extraordinary expenses and sufficient patent revenues are realized, funds are deducted from the pool to repay the extraordinary expenses over several years, thereby amortizing any material impact over a period of time. The Patent Distribution Letter 2018-19 outlines the principles behind this mechanism. Figure 2 includes this as an element to the UC Davis model.

Figure 2. UC Davis Patent Revenue Budget Model

UC Davis Patent Revenue Budget Model (PDF) | Text Alternative

For Net Patent Revenue, patents are assigned based upon the department where the work was done by the Lead Inventor(s) at the time the patent case is recorded. There is no centralized system at UCOP that records this information, so Dean’s Office review for appropriate assignment each year is requested. Patent revenues are to remain with the department where the work was completed and do not follow the Inventor/PI home department or appointment assignments. When there are multiple Lead Inventors, allocations are split according to the proportion of Inventor Share that was paid out in the most recently identifiable payout year. For Research Share, allocations are based upon the inventors and amounts listed in the UCOP Research Share report.

The challenge is in determining, on a patent by patent basis, the amount of Net Patent Revenue to be allocated each year. The key obstacles to calculating the values are:

- Several costs, such as UCOP Operational Costs and General Fund Share, are not recorded at the individual patent case level.

- Deductions for Inventor and Research Shares are netted against the following year’s Net Income for each patent regardless if there is sufficient Net Income.

- Not all patents generate positive net income in a given year; in fact less than half of UC Davis cases produce positive net income.

Consequently, a straightforward activity-based cost accounting for each individual patent case is not reasonable or possible. Therefore, a mechanism was developed to allocate the available Net Patent Revenue pool proportionally to those patents that had positive adjusted net income for the year. Each positive adjusted net income patent is assigned a percentage based upon the proportion of adjusted net income produced relative to the other positive patents. Figure 3 below provides a hypothetical example of the calculations.

Figure 3. Calculation Example for UC Davis Campus Budget Model

Calculation Example for UC Davis Campus Budget Model (PDF) | Text Alternative

Essentially, a patent’s individual adjusted net income is the metric used to split the available net patent revenue pool between income-generating patent Case A (60%) and Case B (40%). As mentioned previously, the model does not allocate the total net income or adjusted net income of an individual patent because UCOP and the campus socialize costs that are not tracked at the individual case level.

Allocations of the Net Patent Revenue are made annually on a one-time basis using COFI fund 99100. High level information can be found in the annual Patent Distribution Letters linked below. Individual department details emailed to Dean/VC Office leadership. Please reach out to your assigned BIA Analyst for additional information.

For more information, contact the Budget Office.

Resources (PDFs):

- Patent Distribution Letter 2025-26

- Adjustment to Patent Budget Model for Investing in the Future of Medicine-February 2026

- Patent Distribution Letter 2024-25

- Patent Distribution Letter 2023-24

- Patent Distribution Letter 2022-23

- Patent Distribution Letter 2021-22

- Patent Distribution Letter 2020-21

UCOP Knowledge Transfer Office